A supporter of the Affordable Care Act (ACA) stands in front of the Supreme Court of the United States as the Court begins hearing arguments from California v. Texas about the legality of the ACA on November 10, 2020 in Washington, DC. Today is the first time that the Court is hearing a case with all three of President Donald Trump's appointments; Associate Justices Neil Gorsuch, Bret Kavanaugh, and Amy Coney Barrett. California v. Texas is the Republican's latest effort to dismantle the Affordable Care Act after repeated efforts to repeal the Act through the legislative process. (Photo by Samuel Corum/Getty Images)

There are a number of changes coming to ACA coverage in 2023. Here’s a breakdown of what enrollees need to know and how to apply.

Enrolling in Affordable Care Act coverage looks a little bit different for 2023, so here’s a breakdown of all the changes and how to enroll for those that need coverage.

How to Enroll

Those interested in enrolling in Affordable Care Act coverage can do so now through Jan. 15, 2023. You must enroll by then to be eligible for 2023 coverage, unless you qualify for a Special Enrollment Period. You can also enroll by Dec. 15 for coverage that starts on Jan. 1, 2023.

If you already know which plan you wish to enroll in, click here, and either select “Take the first step to apply” or “Log in to renew/change plans” and then follow the prompts.

To review plans and prices, click here.

Extended Subsidies to Help Afford Rising Premiums

After four years of premium declines, policies for 2023 are slightly more expensive. But most enrollees won’t feel this increase due to enhanced federal subsidies first implemented as part of Joe Biden’s American Rescue Plan and later extended through this year’s Inflation Reduction Act.

Those enrolled in the benchmark silver plan in the 33 states participating in the federal program will see an average 4% increase in their monthly premium, according to a Department of Health and Human Services report released in October. This year, there was a 3% drop. The remaining states have their own exchanges, for which changes in premium prices vary.

But the Biden administration’s newly-extended subsidies will allow 80% of enrollees to select plans that will cost less than $10 a month and will save these enrollees an average of $800 a year in premiums. Thanks to the Inflation Reduction Act, enrollees will also pay no more than 8.5% of their income on premiums, down from nearly 10%.

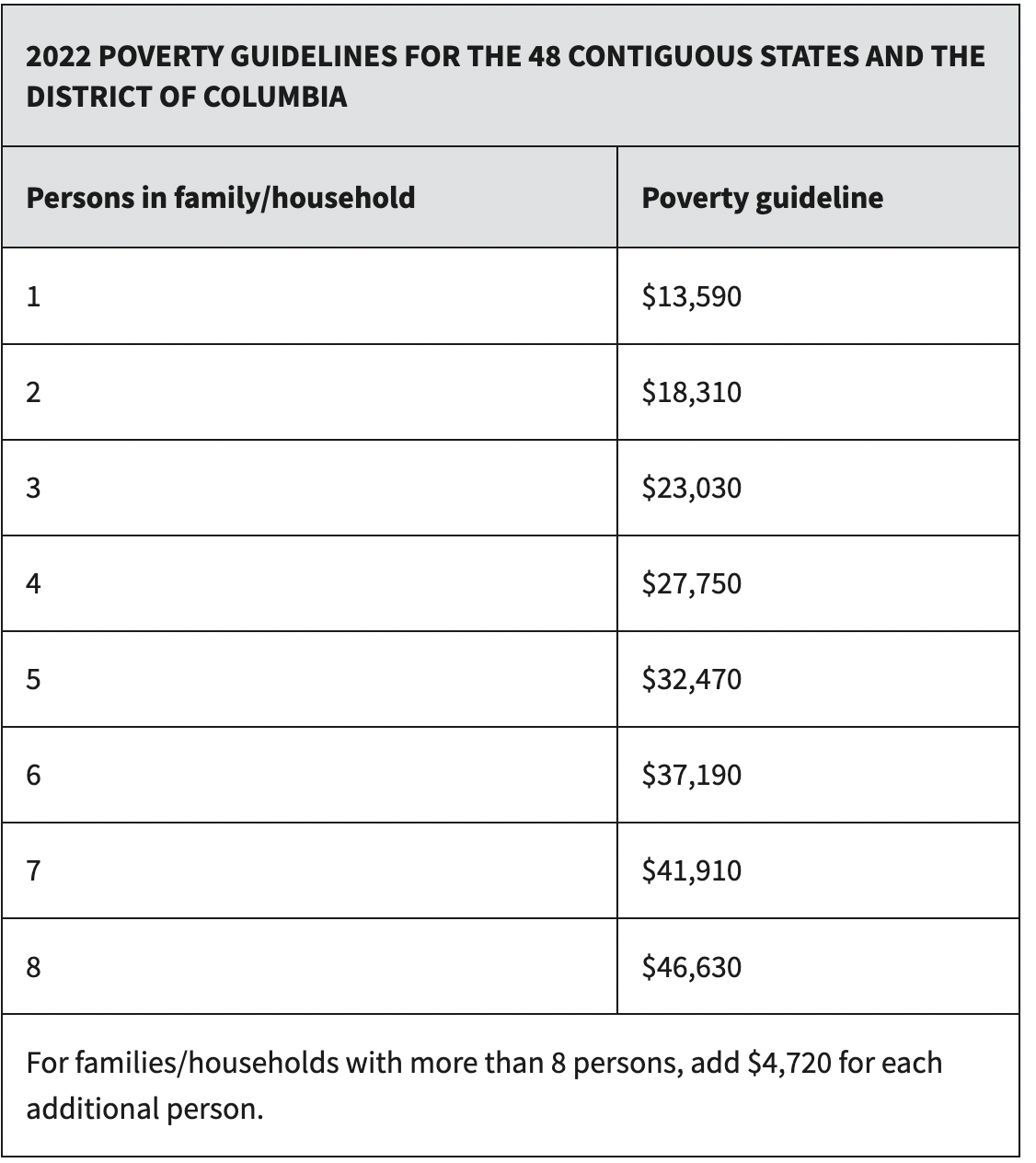

Lower income enrollees will have the opportunity to eliminate their premiums altogether by receiving these subsidies. And for the first time, those earning more than 400% of the federal poverty level—which is most Americans—are eligible for financial help.

More Choices on the Marketplace

More insurers—220 to be exact—are participating in the Affordable Care Act exchange in 2023, which is seven more than were available this year. Additionally, roughly 92% of enrollees will have a choice between at least three insurers, which is up from 89% this year.

Every carrier must also now offer a standardized plan at every metal plan level (Bronze, Silver, Gold, and Platinum), a change meant to simplify the insurance shopping experience. These plans will have a set deductible, out-of-pocket maximum, and copay or coinsurance, which will allow customers to more easily compare other elements of the plans offered, such as premium costs and provider networks. The deductibles for these standardized plans will be higher than in non-standardized policies, but certain benefits, such as primary care and urgent care, will be available pre-deductible.

No ‘family glitch’

Under the ACA, workers who aren’t offered “affordable” insurance coverage—a plan that costs them less than 10% of their income—by their employer are able to receive subsidies to purchase plans on the healthcare exchange. But until now, the ACA didn’t take into consideration how adding family members to employer-sponsored policies could push the cost above what families were able to afford. In these instances, workers and their families haven’t been eligible to get subsidies to buy ACA plans.

But thanks to a new Biden administration rule, family members of workers who are offered affordable individual plans by their employer but unaffordable family plans will be eligible for ACA subsidies in 2023.

About 1 million people will either gain coverage or see reductions in premiums, according to the White House.

Author

Politics

Inside Puerto Rico’s unique role in the US presidential race

Although residents of Puerto Rico can't vote for president in November, they could potentially still influence Electoral College calculations....

Biden makes 4 million more workers eligible for overtime pay

The Biden administration announced a new rule Tuesday to expand overtime pay for around 4 million lower-paid salaried employees nationwide. The...

Local News

Inside Puerto Rico’s unique role in the US presidential race

Although residents of Puerto Rico can't vote for president in November, they could potentially still influence Electoral College calculations....

Biden makes 4 million more workers eligible for overtime pay

The Biden administration announced a new rule Tuesday to expand overtime pay for around 4 million lower-paid salaried employees nationwide. The...